Due Diligence Questionnaire: The Complete Template for Investors

Published on April 2, 2026

Due Diligence Questionnaire: The Complete Template for Investors

A due diligence questionnaire (DDQ) is the structured set of questions investors send to evaluate a fund manager, acquisition target, or vendor before committing capital. This guide covers every section of a complete DDQ template, expert answers to the most common investor questions, and how modern deal teams share DDQs securely.

TLDR: A DDQ is a formal information-gathering document used by institutional LPs, VCs, PE firms, and acquirers to assess risk before a transaction. A standard investor DDQ covers 8-10 sections including firm background, investment strategy, financial performance, legal structure, compliance, operations, cybersecurity, and ESG. Completing one takes 4-10 hours on average. This guide includes a full investor DDQ template and best practices for secure document delivery.

Introduction

Every serious investment conversation eventually arrives at the same moment: the request for a DDQ. Whether you are a fund manager preparing to raise from institutional LPs, a portfolio company being evaluated by a strategic acquirer, or a financial services firm onboarding a new institutional client, a due diligence questionnaire sits at the center of the process.

A DDQ does one thing clearly: it gives the requesting party a structured way to gather the information they need to make a decision. That sounds simple. In practice, it rarely is. A standard 100-question DDQ from an institutional LP takes an average of 4 to 5 hours to complete on the first draft, according to research from Inventive AI. Add follow-up requests and tailored responses and that number climbs fast.

This guide answers the seven most common questions about due diligence questionnaires, includes a full investor-grade DDQ template, and covers how deal teams share sensitive DDQ responses without creating security gaps.

What is a due diligence questionnaire?

A due diligence questionnaire (DDQ) is a formal document one party sends to another to collect structured information as part of a due diligence process. The requesting party uses the responses to evaluate risk, verify representations, and decide whether to proceed with an investment, acquisition, partnership, or business relationship.

DDQs appear across several contexts in finance:

- Institutional LP due diligence: Limited partners (pension funds, endowments, family offices, fund-of-funds) send DDQs to fund managers before committing capital

- M&A buy-side diligence: Acquirers send DDQs to target companies to validate financials, legal structure, and operations

- Vendor risk management: Corporates and financial institutions send DDQs to technology vendors and service providers to assess data security and operational resilience

- Prime brokerage and fund administration: Banks and service providers request DDQs from hedge funds as part of onboarding

According to AIMA, which has published standardized DDQ frameworks since 1997, the DDQ is the industry standard tool for investors conducting due diligence on hedge fund managers. The Institutional Limited Partners Association (ILPA) maintains its own standardized DDQ template that LPs use as a baseline when evaluating private equity managers.

At its core, a DDQ asks one question: Can I trust this firm with my capital? Every question, however technical, traces back to that single concern.

What sections does a due diligence questionnaire cover?

The sections in a DDQ vary by context, but investor-facing DDQs from VCs, PE firms, hedge funds, and family offices typically share a common structure. Here are the core sections most institutional investors expect:

1. Firm Overview and Background Legal name, formation date, ownership structure, registered offices, key principals, AUM, and years in operation.

2. Investment Strategy and Process Target sectors, geographies, deal sizes, sourcing methodology, investment thesis, stage focus (seed, growth, buyout), and portfolio construction philosophy.

3. Team and Key Personnel Partner and senior team bios, tenure, track record per individual, succession planning, team stability (turnover in past 3-5 years), and diversity metrics.

4. Track Record and Performance Fund-by-fund performance data, DPI/RVPI/TVPI by vintage year, benchmark comparisons, attribution analysis, and realization history.

5. Fund Structure and Legal Fund legal structure, GP entity, management company, advisory agreements, fee terms, distribution waterfall, key-man provisions, and LP advisory committee structure.

6. Compliance and Regulatory SEC/FCA/other regulatory registrations, compliance program details, code of ethics, conflict of interest policy, AML procedures, sanctions screening, and FCPA compliance.

7. Operations and Technology Fund administration, custodians, prime brokers, auditors, legal counsel, valuation policy, NAV calculation process, cybersecurity framework, and business continuity plan.

8. Risk Management Portfolio risk monitoring processes, concentration limits, leverage policy, stress testing, and drawdown procedures.

9. ESG and DEI ESG integration in investment decisions, diversity metrics for the investment team, DEI commitments, and UN PRI signatory status.

10. References Current and former LP references, portfolio company contacts, and service provider references.

ILPA's standardized DDQ template covers most of these sections and is widely used as a starting point for LP diligence.

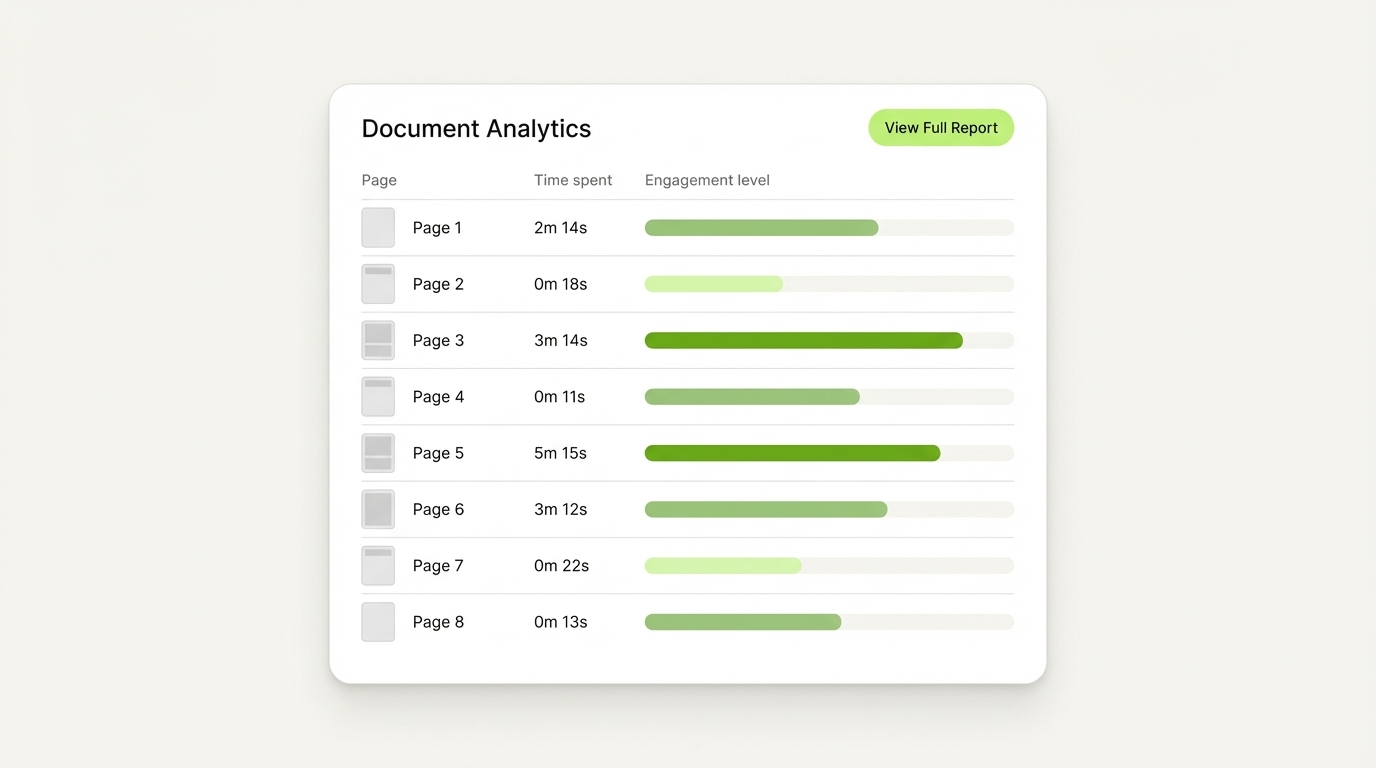

SendNow's document analytics dashboard shows exactly which sections of a DDQ packet investors engaged with most, page by page.

How is a DDQ different from an RFP?

An RFP (Request for Proposal) and a DDQ look similar on the surface but serve fundamentally different purposes.

An RFP is a competitive selection document. A buyer sends it to multiple vendors or managers and uses the responses to choose the best fit for a defined scope. The focus is on capabilities, pricing, and service offerings. The evaluation is comparative.

A DDQ is a risk validation document. The requesting party sends it to assess whether a specific manager, company, or vendor meets baseline requirements for trust, compliance, and operational integrity. It is not a competition. A DDQ asks: Are you safe to work with? An RFP asks: Are you the best fit for this project?

According to DiligenceVault, asset managers receive DDQs, RFPs, RFIs, and 15(c) questionnaires throughout the year, and each requires a distinct operational approach. Responding to a DDQ as if it were an RFP is a common error that can slow the process or signal a lack of institutional sophistication to the investor.

The practical difference: an RFP compares you to others. A DDQ validates you on your own.

How long does it take to complete a due diligence questionnaire?

The time to complete a DDQ depends on three factors: the number of questions, the availability of source materials, and how tailored the responses need to be.

A standard 100-question institutional DDQ takes an average of 4 to 5 hours for a first draft, with more time required for responses customized for a specific LP's focus areas, according to Inventive AI. Extended follow-up requests can add additional rounds of work.

For fund managers going through a formal fundraise from institutional LPs, the timeline looks roughly like this:

- Weeks 1-2: Initial DDQ submission (50-150 questions, document package)

- Weeks 3-4: Follow-up questions and clarifications

- Weeks 5-8: On-site or virtual management meetings, reference checks

- Weeks 9-12+: Final investment committee review and decision

For M&A scenarios, the full due diligence process typically runs 6-12 weeks after a letter of intent is signed, depending on deal size and complexity, according to Veritext. The DDQ is often the opening document request in that process.

The most common ways fund managers reduce DDQ response time: building a pre-populated DDQ library, maintaining up-to-date track record data, and using a structured platform to share the completed DDQ and supporting documents securely with each LP.

What questions do investors typically include in a DDQ?

Across VC, PE, and hedge fund contexts, institutional investors ask a consistent set of high-priority questions. Here are the categories and representative examples:

Firm and team credibility

- How many investment professionals are currently on the team and in what roles?

- What is the average tenure of the investment team?

- Has any key person left the firm in the past three years? If so, under what circumstances?

- Is there a formal succession plan in place?

Strategy and edge

- What is your sourcing strategy and how do you identify proprietary deal flow?

- How do you assess a company's competitive position before investing?

- What distinguishes your investment process from peers in your strategy?

Track record and performance

- What is the net IRR, DPI, RVPI, and TVPI for each fund by vintage year?

- How does performance compare to the relevant benchmark?

- Which individual investments have driven the most value creation, and why?

- Are there any investments where you wrote the position down to zero?

Operations and compliance

- Is the firm registered with the SEC (or relevant regulator) and in good standing?

- Describe your cybersecurity policies and any data breach history.

- What is your valuation methodology for unrealized investments?

- Do you have a whistleblower policy and an independent compliance officer?

ESG and DEI

- What percentage of the investment team identifies as women or from underrepresented groups?

- Is the firm a signatory to the UN Principles for Responsible Investment (PRI)?

- How does ESG factor into your investment thesis and portfolio monitoring?

The VC Lab complete LP DDQ guide notes that institutional LPs can ask 50 or more questions covering strategy, team, track record, fund structure, risk management, and operations in a single diligence process.

SendNow tracks which pages of your DDQ packet investors spend the most time on, so you know exactly where their attention lands before the follow-up conversation.

What does a standard investor DDQ template look like?

Below is a condensed investor DDQ template structured for fund managers responding to institutional LPs. Use it as a starting point and adapt it to your specific fund strategy and investor type.

DUE DILIGENCE QUESTIONNAIRE TEMPLATE Prepared by: [Fund Manager Name] Prepared for: [Investor / LP Name] Date: [Date] Fund: [Fund Name and Vintage] Classification: Confidential

Section 1: Firm Overview

- 1.1 Legal name of the management company and general partner entity

- 1.2 Date of formation and jurisdiction of incorporation

- 1.3 Registered address and all office locations

- 1.4 Ownership structure of the management company (include org chart)

- 1.5 Is the firm a registered investment adviser? If yes, provide CRD number and date of registration

- 1.6 Total assets under management (current and historical by year)

- 1.7 List all funds managed by the firm with vintage year, target size, and close date

Section 2: Investment Team

- 2.1 List all investment professionals with name, title, years at firm, and prior experience

- 2.2 Has any partner or senior investment professional departed in the past five years? If yes, provide circumstances

- 2.3 What is the investment team's ownership structure in the management company and GP?

- 2.4 Are formal non-compete and non-solicit agreements in place for all partners?

- 2.5 Describe the firm's succession plan for the loss of a key principal

- 2.6 Provide DEI metrics for the investment team (gender, ethnicity, educational background)

Section 3: Investment Strategy

- 3.1 Describe your investment strategy, including target sectors, geographies, and deal stages

- 3.2 What is your typical initial check size and ownership target at entry?

- 3.3 How does the firm source proprietary deal flow? What percentage of deals are proprietary vs. intermediary-sourced?

- 3.4 Describe your investment decision-making process, including how the investment committee operates

- 3.5 What is your portfolio construction philosophy? How many positions does a fund typically hold?

- 3.6 Describe your value-add model post-investment

Section 4: Track Record

- 4.1 Provide a complete fund performance table: fund name, vintage year, committed capital, invested capital, realized value, unrealized value, total value, net IRR, net DPI, net RVPI, net TVPI

- 4.2 Provide a full portfolio company list for each fund with entry date, entry valuation, current status, and realized/unrealized value

- 4.3 What are your five best-performing and five worst-performing investments? Provide brief attribution for each

- 4.4 Has any portfolio company filed for bankruptcy or been written to zero? If yes, explain

- 4.5 How does your net IRR compare to the Cambridge Associates or Preqin benchmark for your vintage year and strategy?

Section 5: Fund Terms and Structure

- 5.1 What is the target fund size and hard cap for the current fund?

- 5.2 Management fee rate and basis (committed or invested capital, and during what periods)

- 5.3 Carried interest rate and hurdle rate

- 5.4 Is there a GP commitment? What percentage of total fund size?

- 5.5 Describe the distribution waterfall (European vs. American carry)

- 5.6 What are the key-man provisions and trigger events?

- 5.7 Is there an LP Advisory Committee? What rights does it have?

- 5.8 What are the LP consent rights for material fund changes?

Section 6: Legal, Compliance, and Regulatory

- 6.1 Has the firm or any principal ever been subject to regulatory investigation, censure, or fine?

- 6.2 Describe the firm's compliance program structure and who is responsible for compliance oversight

- 6.3 Does the firm have a code of ethics and conflict of interest policy? (Provide copies upon request)

- 6.4 Describe the AML and KYC procedures for LP onboarding

- 6.5 Does the firm have FCPA compliance policies and procedures in place?

- 6.6 Has the firm ever experienced a material cybersecurity incident? If yes, describe

- 6.7 What cyber insurance coverage does the firm carry?

Section 7: Operations

- 7.1 Name the fund administrator, auditor, legal counsel, and prime broker/custodian

- 7.2 Describe the valuation policy for unrealized investments and who approves quarterly valuations

- 7.3 What is the firm's business continuity and disaster recovery plan?

- 7.4 What technology platforms does the firm use for portfolio monitoring, fund accounting, and LP reporting?

- 7.5 Describe the LP reporting cadence (quarterly letters, capital account statements, K-1s, etc.)

Section 8: Risk Management

- 8.1 What are the portfolio's concentration limits by company, sector, and geography?

- 8.2 How does the firm monitor and manage portfolio risk on an ongoing basis?

- 8.3 Describe the firm's process for making follow-on investment decisions

- 8.4 Has any fund ever had a capital call default or clawback event? If yes, describe

Section 9: ESG

- 9.1 Is the firm a signatory to the UN Principles for Responsible Investment (PRI)?

- 9.2 How does the firm integrate ESG factors into the investment process?

- 9.3 Describe any ESG-related exclusions or restrictions in the fund's investment mandate

- 9.4 What DEI commitments has the firm made at the firm and portfolio level?

Appendix: Documents Requested

- Audited financial statements for all funds (past 3 years)

- Form ADV Part 1 and Part 2A (if registered investment adviser)

- LP Agreement and side letter template

- Sample quarterly LP report

- Organizational chart (firm and fund entities)

- Principal biographies

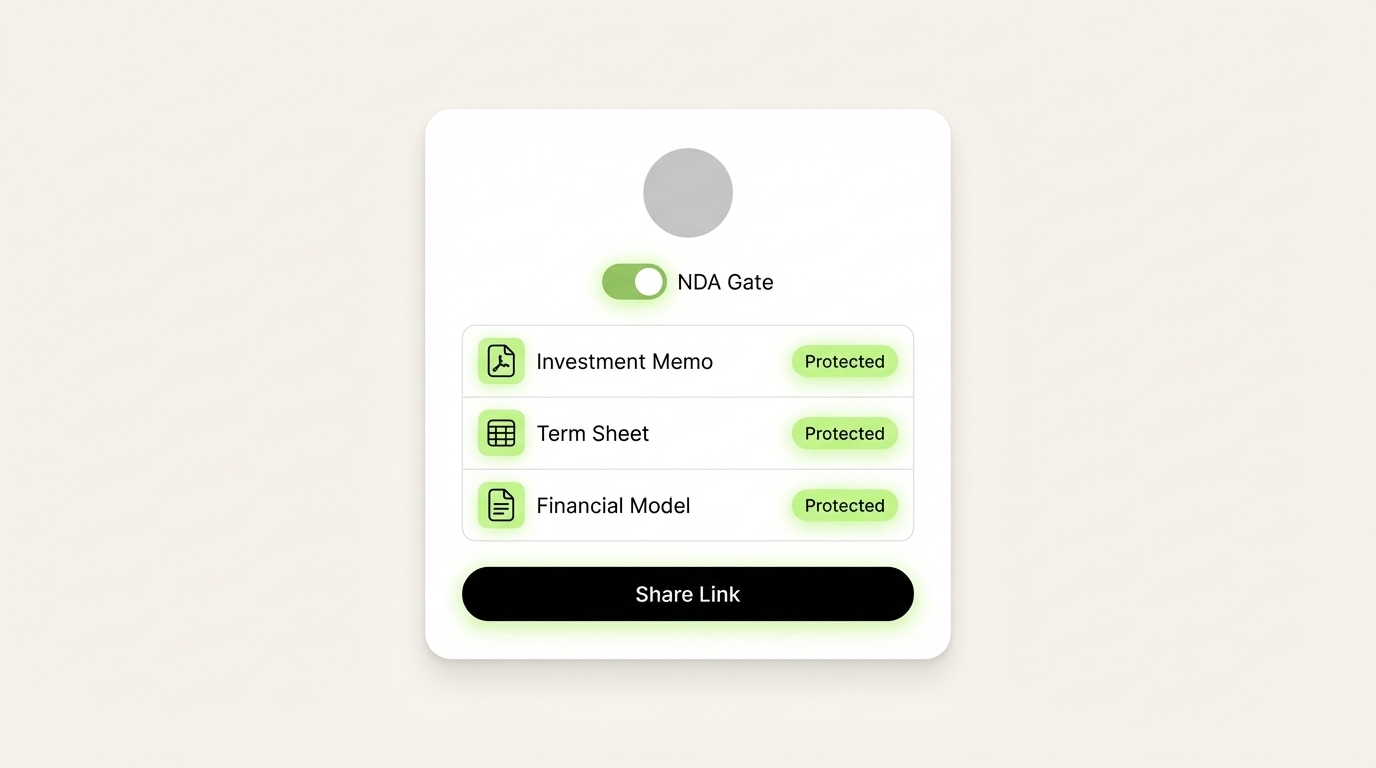

Platforms like SendNow let fund managers share their completed DDQ packets with institutional LPs inside a branded, NDA-gated deal room, with full visibility into who accessed which documents and when.

How do deal teams share DDQs securely?

Sharing a due diligence questionnaire with institutional investors creates a real document security problem. DDQ responses contain sensitive firm data: performance history, portfolio details, compliance records, and personal information about team members. Email is inadequate. Unprotected Google Drive or Dropbox links create audit gaps, and they give you no visibility into who accessed which documents or when.

Best practices for secure DDQ document sharing:

1. Use a dedicated secure link, not email attachments. A secure document link gives you control over access, expiry, and permissions. It also creates an audit trail the investment process requires.

2. Require NDA acceptance before access. For institutional LP processes, every viewer should formally acknowledge confidentiality before they see any data. This is standard practice and builds credibility with sophisticated investors.

3. Enable page-level analytics. Understanding which sections of your DDQ packet investors spend the most time on - and which they skip - gives you valuable intelligence for follow-up conversations. If an LP spent 12 minutes on your track record section and 30 seconds on team bios, you know exactly what to address in the next meeting.

4. Apply dynamic watermarks. Watermarking every page of the DDQ with the viewer's name and timestamp discourages unauthorized screenshots and sharing, and protects you if data surfaces outside the process.

5. Enable screenshot protection. For the most sensitive materials (financial performance data, term sheets), screenshot-blocking technology prevents digital or physical capture of confidential data.

SendNow is purpose-built for this workflow. It gives fund managers and deal teams a branded deal room where each LP receives a secure, NDA-gated link to the complete DDQ package. Real-time open notifications tell you the moment an investor opens the document, and page-by-page analytics show exactly which sections they reviewed. Dynamic watermarks, AES-256 encryption, and screenshot protection keep sensitive data secure throughout the diligence process.

SendNow's NDA-gated deal room lets fund managers control who sees their DDQ materials and when, with a full audit trail of every view and page interaction.

Conclusion

A due diligence questionnaire is not a formality. It is often the single document that determines whether an institutional LP moves forward with a fund commitment. The quality of your responses, the organization of your supporting documents, and the professionalism of your delivery all signal credibility before the relationship formally begins.

Use the template in this guide as a baseline, adapt it to your fund strategy and investor type, and keep your responses current between fundraises. The fund managers who win institutional capital fastest are almost always the ones who already have their DDQ materials organized, current, and ready to share at a moment's notice.

When you are ready to share your DDQ with investors, SendNow gives you a secure, analytics-enabled platform built specifically for financial professionals handling sensitive deal documents. Start your free trial at sendnow.live, no credit card required.

Keep Reading

- M&A Due Diligence Checklist: The Full 2026 Guide

- A complete guide to private equity due diligence: the five types PE investors run, what they examine in financials and operations, red flags that kill deals, and how to prepare your company for a successful transaction.

- NDA Best Practices for Sharing Confidential Financial Documents

- What Is a Virtual Data Room? Complete Guide for Finance Professionals