A complete guide to private equity due diligence: the five types PE investors run, what they examine in financials and operations, red flags that kill deals, and how to prepare your company for a successful transaction.

Published on April 2, 2026

A complete guide to private equity due diligence: the five types PE investors run, what they examine in financials and operations, red flags that kill deals, and how to prepare your company for a successful transaction.

Private Equity Due Diligence: What Investors Look For

TLDR

- PE due diligence covers five core areas: commercial, financial, legal, management/operations, and IT

- The average PE firm reviews 80 opportunities for every one investment it makes

- A Quality of Earnings (QoE) report is the central piece of financial due diligence in any PE deal

- PE diligence is fundamentally different from VC diligence in focus, depth, and what constitutes a red flag

- The companies that close PE deals fastest prepare their data rooms and resolve issues before going to market

Introduction

Private equity firms invest with precision. Before they commit to a deal, they put every assumption to the test.

The average PE firm reviews 80 companies for every one it invests in, according to Affinity. A single deal takes an average of 20 meetings, four rounds of negotiation with the target company, and 3.1 full-time deal team members. That ratio makes it plain: PE due diligence is not a courtesy review. It is a structured, high-stakes examination designed to either confirm an investment thesis or kill a deal before capital is deployed.

This guide breaks down what PE investors actually look for, the five categories of diligence they run, the documents they want to see, the red flags that cause them to walk away, and how sellers can prepare for the process effectively.

Table of Contents

- What Is Private Equity Due Diligence?

- What Do PE Investors Look For in Financials?

- PE vs. VC Due Diligence: Key Differences

- What Is a Quality of Earnings Report?

- The Five Types of Due Diligence in Private Equity

- Red Flags PE Investors Look For

- How Long Does PE Due Diligence Take?

What Is Private Equity Due Diligence? {#what-is-pe-due-diligence}

Private equity due diligence is the systematic investigation a PE firm conducts on a target company before an investment or acquisition. Its purpose is to verify that information the company presents is accurate, uncover hidden risks and liabilities, and establish a fair purchase price grounded in what is actually true about the business.

According to Carta, PE due diligence runs in two phases. The first is exploratory: the deal team checks whether the company fits the fund's investment thesis at a fundamental level. Companies that pass this initial screen move to the confirmatory phase, where the team engages lawyers, accountants, and third-party consultants to validate every major claim and assumption with independent verification.

Unlike public companies, which must disclose extensive information to regulators and the market, private companies have far fewer public data requirements. This makes PE due diligence more demanding, since deal teams must request, verify, and interpret information that has no public record. A confidential information memorandum (CIM), provided by the seller, usually serves as the starting point, but experienced deal teams treat the CIM as a hypothesis to test, not a conclusion to accept.

As of early 2026, global PE dry powder has surged to $2.59 trillion, with the U.S. market alone accounting for a record $1.1 trillion of unallocated capital, per Affinity. More capital chasing a finite set of quality assets means deal teams work harder to find proprietary opportunities and conduct diligence faster without sacrificing rigor.

What Do PE Investors Look For in Financials? {#pe-financial-due-diligence}

Financial due diligence is the highest-priority workstream in most PE deals. The deal team first confirms the accuracy of the target company's financial statements, then digs into the performance drivers that do not always appear on the face of the accounts.

Core Financial Documents Requested

- Income statement, balance sheet, and cash flow statement (3-5 years historical, monthly granularity)

- Financial projections (3 years forward with detailed assumptions)

- Bank statements reconciled against financial statements

- Accounts receivable and payable aging schedules

- Product-level and customer-level gross margin analysis

- Customer contract value, average contract length, and churn rate

- Customer acquisition cost and customer lifetime value

- Audited accounts (standard requirement at larger deal sizes)

- Any venture debt, lines of credit, or outstanding loans with full terms

The Quality of Earnings Analysis

The most important financial exercise in any PE deal is the Quality of Earnings (QoE) report, usually prepared by an independent accounting firm. A QoE digs behind reported EBITDA to assess whether earnings are real, recurring, and sustainable. It identifies one-time items that inflate profitability, revenue recognition practices that pull forward future revenue, and customer concentration risks that could evaporate if a single contract ends.

Affinity describes the QoE as a stress-test: what would earnings look like if the two largest customers canceled their contracts? What would working capital requirements look like in a downturn? That kind of scenario analysis is standard practice for any serious deal team.

The deal team also analyzes working capital requirements, which determine how much cash the business needs to operate, and capital expenditure intensity, which determines how much reinvestment the business demands to sustain growth.

PE vs. VC Due Diligence: Key Differences {#pe-vs-vc}

The core distinction is what each type of investor attempts to validate.

Venture capital investors back companies at early stages, where financial history is thin and the key question is whether the founding team can build something large. VC due diligence focuses primarily on the founding team, product quality, market size, and the plausibility of the growth thesis. Financials matter but are often projections rather than history. Affinity describes VC firms as looking for strong founders and strong company performance.

Private equity investors typically target more mature companies with established revenue, paying customers, and existing management teams. PE due diligence is fundamentally financial in nature, since the investment thesis often centers on improving the company's profitability and engineering a return at exit. PE investors look for companies where they can create value, which sometimes means looking for fixable problems rather than flawless performance.

A second key difference is leverage. Because many PE deals use debt financing, the target company's cash flow stability, debt capacity, and ability to service interest payments are critical inputs that are irrelevant in a typical VC deal.

A third difference is the CIM. PE deals involve a formal confidential information memorandum from the seller. VC deals rely primarily on pitch decks and founder conversations, with formal diligence materials assembled only after initial interest is established.

What Is a Quality of Earnings Report? {#quality-of-earnings}

The Quality of Earnings report is a detailed financial analysis, usually prepared by an independent accounting firm on behalf of the PE buyer, that assesses the reliability and sustainability of a target company's reported earnings.

A standard QoE covers:

- Adjusted EBITDA reconciliation: Removes one-time items, non-recurring costs, and owner-specific expenses that inflate reported profitability

- Revenue recognition review: Confirms revenue is recognized in line with contract terms and accounting standards, with no premature recognition

- Customer concentration analysis: Identifies what percentage of revenue comes from the top 3-5 customers and the risk profile of those relationships

- Working capital normalization: Establishes the true baseline of working capital needed to run the business at steady state

- Off-balance-sheet liability identification: Uncovers commitments, guarantees, or contingent liabilities not reflected in financial statements

- Cash flow sustainability assessment: Tests whether free cash flow can support debt service if leverage is applied

Plante Moran identifies the QoE as one of the seven most critical steps in a PE acquisition, particularly for platform deals where the buyer plans to use the target as a base for add-on acquisitions.

Sellers who engage a sell-side QoE advisor before going to market reduce deal uncertainty significantly. A clean, pre-verified QoE removes one of the most common reasons buyers revise their price downward after confirmatory diligence.

The Five Types of Due Diligence in Private Equity {#five-types}

Every PE firm has its own process, but five categories of diligence appear in virtually every institutional deal.

1. Commercial Due Diligence

Commercial due diligence examines the industry and the target company's position within it. Because PE investment goals are often financial rather than strategic, some firms hire outside advisors or industry experts to assess markets they do not know well internally.

Key evaluation areas:

- Market size and growth trajectory

- Competitive position and defensibility of market share

- Customer base depth and churn risk

- Sales volume by product or service line

- Supplier base stability

- Pricing power and product differentiation

- Revenue model sustainability

Key questions: Is this market growing or contracting? Does the company have durable competitive advantages? What is the realistic ceiling on growth given competitive dynamics?

2. Financial Due Diligence

Financial due diligence verifies the accuracy of financial statements, analyzes the quality and sustainability of earnings through the QoE process, and models the company's future cash flows under multiple scenarios.

Key questions: Are the reported earnings real and recurring? What does normalized EBITDA look like once one-time items are removed? How much working capital does the business consume each cycle?

3. Legal Due Diligence

Legal due diligence examines the company's legal structure, contracts, compliance status, intellectual property portfolio, and any pending or potential litigation. It also addresses the consequences of a change of ownership, including change-of-control provisions in customer and supplier contracts that may allow counterparties to exit relationships after a sale.

Key questions: Are there undisclosed liabilities? Does the company comply with applicable regulations in all jurisdictions where it operates? Are there material contracts that terminate on a change of control?

4. Management and Operational Due Diligence

Operational due diligence evaluates the quality of the management team, the efficiency of day-to-day operations, and the opportunities for the PE firm to create measurable value after acquisition.

Problems found here are not automatic deal-killers. An underperforming management team or inefficient operations can give a skilled PE sponsor a clear value creation lever, potentially at a more attractive purchase price. Spotting these issues during diligence converts them from risks into opportunities.

Key evaluation areas:

- Organizational structure and reporting lines

- Management team background, track record, and alignment with post-acquisition goals

- Operational processes and documentation

- Identification of unprofitable product lines

- Potential new sales and marketing channels

- Technology that could reduce capital expenditure if upgraded

Key questions: Is the management team capable of executing the post-acquisition plan? Are there operational inefficiencies the firm can resolve? Is there dangerous key-person dependency?

5. Technology and IT Due Diligence

IT diligence assesses the company's technology infrastructure, cybersecurity posture, software systems, data management practices, and scalability. In tech-enabled businesses, this workstream can be as intensive as the financial review.

Key evaluation areas:

- Current software and hardware inventory

- ERP, CRM, financial systems, and their integration

- Data management and security practices

- Cybersecurity policies, incident history, and vulnerability assessment

- IT staff capability and dependency on third-party vendors

- Disaster recovery and business continuity planning

- Scalability of current infrastructure against the post-acquisition growth plan

Key questions: Is the technology scalable without a major capital injection? Are there active cybersecurity vulnerabilities? Does the business rely on legacy systems that create operational risk?

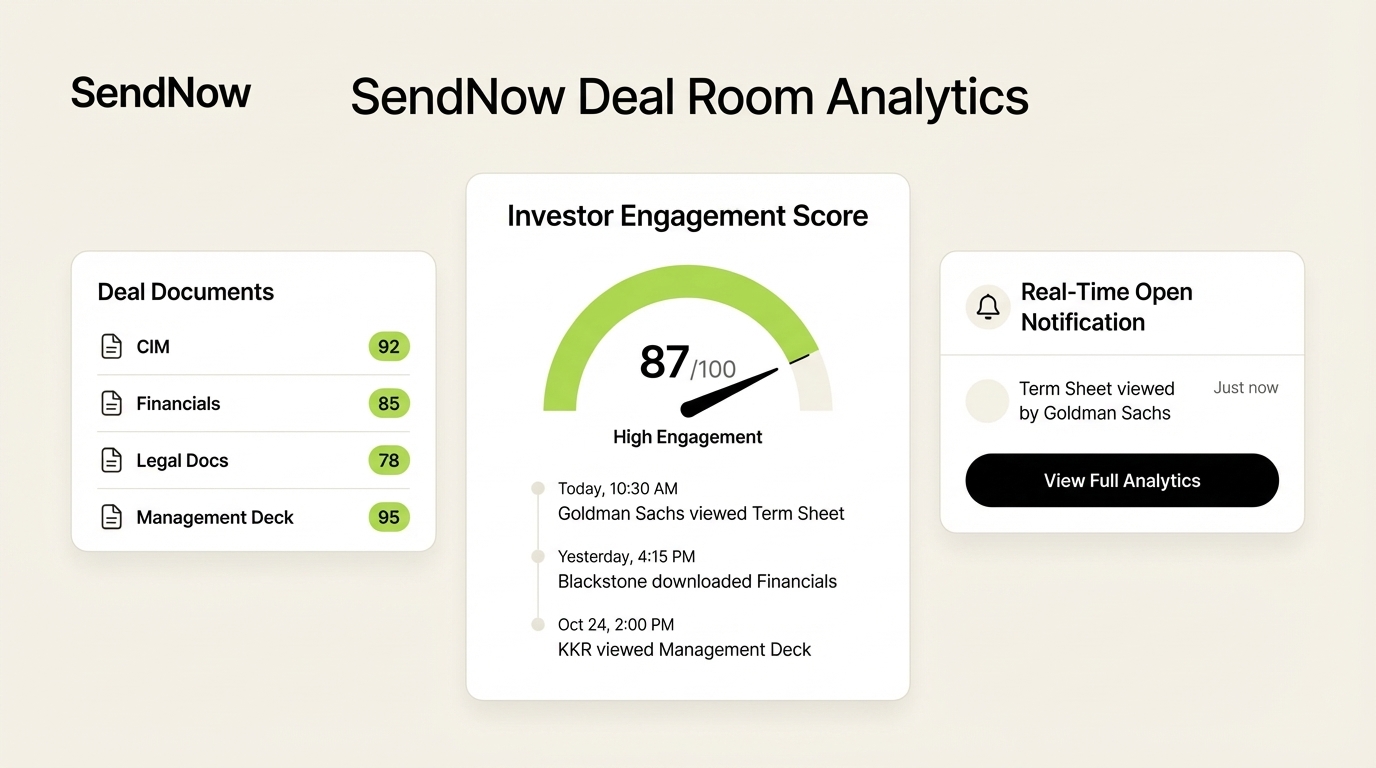

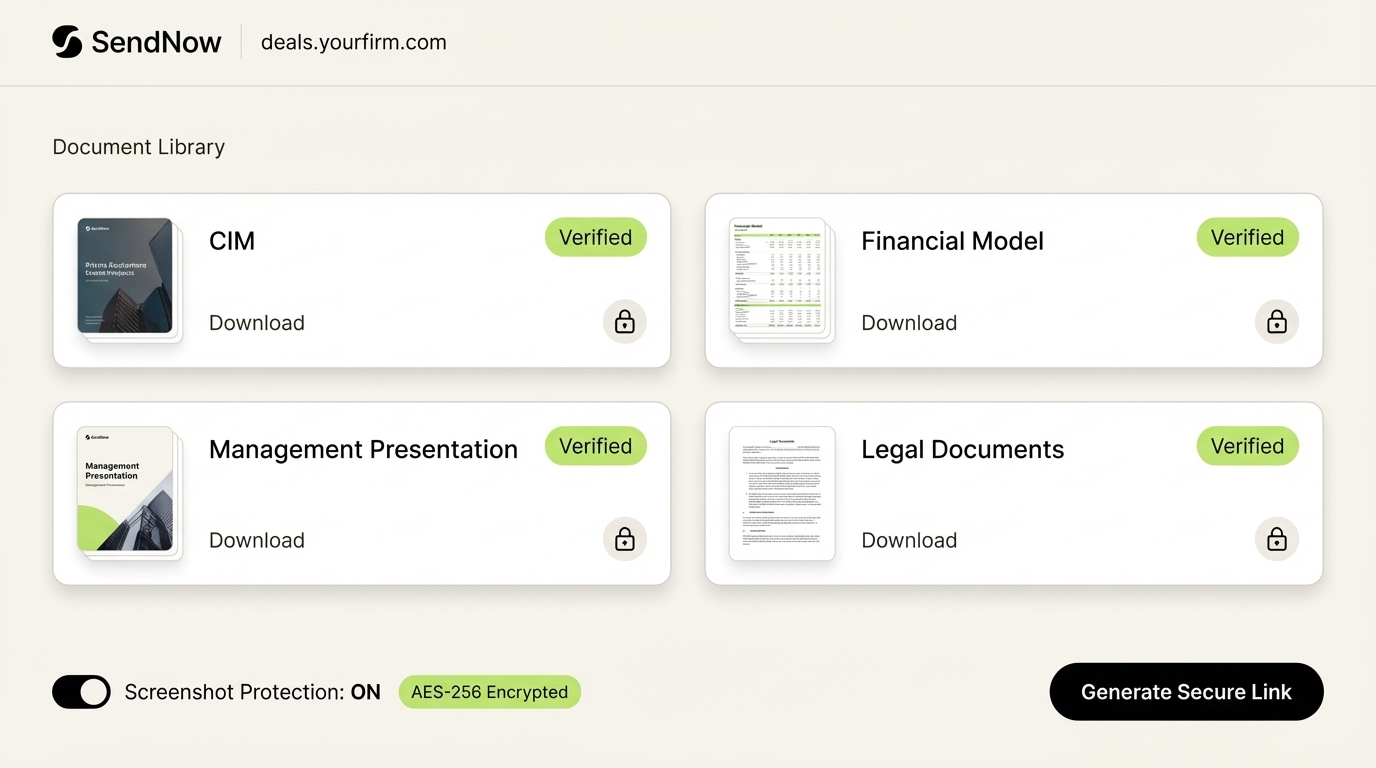

Companies that organize their diligence materials in a purpose-built platform before the process starts communicate preparedness from the first meeting. SendNow gives sellers a branded deal room with AES-256 encryption, screenshot protection, dynamic watermarks, and NDA gating on sensitive documents. Page-by-page analytics reveal exactly which sections of the CIM, financial model, or management presentation the deal team reviewed most carefully, giving sellers a significant advantage in every follow-up conversation.

Red Flags PE Investors Look For {#red-flags}

Experienced deal teams know what trouble looks like before it announces itself. These are the categories of red flags that most commonly slow or kill deals.

Financial Red Flags

- Revenue growth that does not reconcile with cash actually collected

- High customer concentration: top 3 customers represent 70% or more of total revenue

- Declining gross margins not explained by a documented, intentional pricing strategy

- Undisclosed related-party transactions or loans from owners

- Deferred revenue recognized earlier than contractually supported

- Accounts receivable aging that shows large balances past 90 days without explanation

- EBITDA that looks strong on paper but weak after removing owner-specific perks and one-time items

Legal and Compliance Red Flags

- Pending litigation or regulatory investigations not disclosed in the CIM

- Missing IP assignment agreements from key contributors

- Open correspondence with tax authorities suggesting audit exposure

- Material contracts with change-of-control termination clauses

- Regulatory violations in the company's core operating jurisdiction

Management Red Flags

- Key person dependency: the CEO controls all major customer relationships personally, with no documented succession path

- High management turnover in the 12 to 24 months before sale

- Management compensation structures that are entirely misaligned with PE ownership economics

- Founders unclear or evasive about their role intentions post-acquisition

Operational Red Flags

- No documented processes; the business runs on institutional knowledge held by one or two people

- IT infrastructure requiring significant capital investment before it can support growth

- Customer relationships managed entirely through one salesperson with no CRM record

- Vendor concentration risk comparable to customer concentration risk

NMS Consulting frames this well: PE due diligence is a decision tool that determines what is true, what is risky, what creates value, and what to do about it. Red flags are inputs to that decision, not automatic disqualifiers. A firm that spots a fixable problem during diligence can price it into the deal and convert it into a value creation opportunity post-close.

How Long Does Private Equity Due Diligence Take? {#timeline}

PE due diligence typically runs 60 to 90 days from the execution of a letter of intent (LOI) to closing. For smaller, cleaner deals, it can complete in 45 days. For complex platform acquisitions with multiple jurisdictions, regulatory requirements, or contested issues, it can extend to 120 days or more.

The timeline depends on several factors:

| Factor | Effect on Timeline |

|---|---|

| Completeness of seller materials at outset | Largest single variable; incomplete materials add weeks |

| Company financial and legal complexity | More complexity means more workstreams running in parallel |

| Third-party engagement (auditors, IP attorneys, environmental consultants) | Third-party scheduling is often outside the deal team's control |

| Negotiation dynamics around price and terms | Contested QoE findings or working capital disagreements slow the process |

| Number of jurisdictions involved | International deals require multi-jurisdiction legal and tax review |

According to E78 Partners, deals that stall most often do so because the seller was not prepared, not because the buyer was slow. Companies that pre-populate their data rooms, resolve outstanding legal issues before going to market, and engage experienced M&A advisors close significantly faster than those that begin preparation after signing the LOI.

The most controllable variable in the entire PE due diligence process is preparation quality on the sell side.

Conclusion

Private equity due diligence is the most thorough examination a private company ever faces. It tests financials, operations, legal compliance, management quality, and technology infrastructure simultaneously. The companies that survive that examination in good shape, and close on favorable terms, do so because they prepared long before the process formally began.

A well-organized data room, clean financial statements, resolved legal issues, and documented operations are not advantages. They are the baseline expectation of any sophisticated buyer.

If you are preparing a company for PE sale or need a secure platform for your deal room, SendNow offers branded deal rooms with NDA gating, dynamic watermarks, AES-256 encryption, screenshot protection, and AI engagement scoring. The Business plan starts at $33 per month for teams of up to three members. Start your free trial with no credit card required.