Series A Due Diligence: Document Checklist for Founders

Published on April 2, 2026

Series A Due Diligence: Document Checklist for Founders

TLDR

Series A due diligence is a structured document review process that happens after a VC expresses serious interest. Investors request corporate records, financial statements, IP documentation, cap table details, material contracts, and employee agreements — all organized in a secure data room. Founders who prepare this material before receiving a term sheet cut up to a week off their closing timeline. This guide covers every document category, explains what VCs actually look for in each one, and shows you how to manage the process securely and professionally.

Introduction

Most founders treat due diligence like something that happens after a term sheet. That instinct costs time and, sometimes, the deal itself.

Due diligence begins earlier than founders expect. Escalon Services' investor preparation guide puts it plainly: "Diligence begins the moment an investor starts asking second-level questions. If your answers are slow, inconsistent, or incomplete, the investor does not only learn about your business. They learn about your operational maturity."

The solution is preparation before the process starts. A well-organized, complete data room signals to investors that you run a disciplined company. A chaotic, incomplete data room signals the opposite — and gives investors reasons to slow down or walk away.

This guide organizes the full Series A due diligence document checklist into seven question-driven sections, drawing on Y Combinator's official diligence checklist, Underscore VC's data room best practices, and practitioner guidance from institutional investors.

Table of Contents

- What documents do investors ask for in a Series A?

- How long does Series A due diligence take?

- What is a Series A data room?

- What financial documents do founders need for Series A?

- What legal documents are required for Series A due diligence?

- How do you organize a due diligence data room?

- What is the difference between a pitch deck and a due diligence data room?

What documents do investors ask for in a Series A?

The canonical reference for Series A diligence documents comes from Y Combinator. YC's Series A diligence checklist, compiled by YC Continuity's General Counsel Jason Kwon after involvement in hundreds of financings, organizes requests into seven major categories:

1. Corporate Records and Charter Documents

- All minutes of directors' and stockholders' meetings and written consents

- Certificate of Incorporation, Certificates of Designation, and Bylaws

- Corporate organizational chart if there are parents or subsidiaries

2. Business Plan and Financials

- Current business plan and financial projections

- Most recent financial statements (income statement, balance sheet, cash flow)

3. Intellectual Property

- List of trademarks, patents, copyrights, and domain names with filing or registration documentation

- IP assignment agreements if any IP was assigned to the company from a founder, prior employer, or contractor

4. Security Issuances and Cap Table

- Full stockholder list with issuance dates and original prices

- Option holder list with grant dates and exercise prices

- All agreements relating to outstanding options, warrants, and conversion rights

- Vesting schedules for all stock and options, including acceleration provisions

- Evidence of federal and state exemption compliance (including Rule 701)

5. Material Agreements

- Terms of service / terms of use for customers

- All contracts involving obligations or payments above $25,000

- Property leases (personal and real)

- Debt instruments, mortgages, and encumbrances

- Insurance policies

- Partnership, joint venture, and consulting agreements

- Any agreements requiring third-party consents connected to the financing

6. Disputes and Potential Litigation

- Any pending or threatened legal actions or regulatory investigations

- Correspondence relating to alleged IP infringement by the company

- Any labor disputes or union actions

7. Employees and Benefits

- Full employee and consultant list: title, salary, bonus structure, classification, state of residence

- Standard offer letter template

- All agreements with officers and directors that include severance or acceleration provisions

- Equity plan documents: option agreements, notice of exercise, stock purchase agreements

- 401(k) plan documents and Form 5500 filings for the last three years

- Employee handbook

YC's note on timing is worth quoting directly: "Having all of this together in one place — a Data Room — before you sign a term sheet will cut as much as a week off of your closing process."

How long does Series A due diligence take?

The realistic answer: 4 to 8 weeks after a term sheet is signed, though poorly organized data rooms can extend this to 12 weeks or more.

Qubit Capital's due diligence timing analysis puts the funnel in stark terms: for every 101 opportunities a VC reviews, roughly 28 reach management meetings, about 5 reach full diligence, and only one gets funded. The selectivity of the process means that when a VC commits to full diligence, they move deliberately.

The timeline typically breaks down as follows:

| Phase | Duration | What Happens |

|---|---|---|

| Initial review | 1-2 weeks | VC reviews pitch deck and financial summary |

| Partner pitch | 1-2 weeks | Full team presentation, initial data room access |

| Term sheet negotiation | 1-2 weeks | Offer, counter, and signature |

| Legal diligence | 3-6 weeks | Lawyers review all corporate, legal, and financial documents |

| Closing | 1-2 weeks | Final documents, wire transfer |

Founders who prepare their data room before fundraising starts compress the legal diligence phase significantly. Alexander Jarvis's due diligence request list notes that most delays come not from investors being slow but from founders scrambling to locate documents that should have been organized months earlier.

The biggest time killers:

- Missing board consent minutes — Often undocumented for early decisions

- Equity grants without proper 409A coverage — YC explicitly warns founders to clear any pending equity grants before starting a raise because a term sheet triggers a material event that may affect 409A valuation

- Contracts that require third-party consent — Customers or partners who have co-sale rights, change-of-control provisions, or anti-assignment clauses need to be identified and managed early

- Disorganized IP assignments — Especially common when founders wrote early code at a prior employer or as contractors

What is a Series A data room?

A Series A data room is a secure, organized digital repository of the documents an investor needs to complete due diligence before wiring capital. It is different from an early-stage pitch folder — it is more comprehensive, more legally significant, and more sensitive.

UseHaven's data room guide describes the function accurately: "It's your company's organized truth — every file investors will want to see before wiring real money. Done right, it tells them, 'we run this company like adults.' Done poorly, it can stall a round for weeks."

A data room exists at two stages in the fundraising process:

Pre-term sheet data room: Shared with serious investors at the partner pitch stage. Contains the pitch deck, team bios, product overview, financial summary, and cap table. It answers strategic and financial questions without providing full legal access.

Post-term sheet data room: Shares the complete YC-style document checklist with investors' legal counsel. Contains all corporate documents, full financials, IP records, and legal agreements. This is the legal diligence environment.

The distinction matters because what you share, and when, shapes the conversation. Underscore VC's data room guide frames it well: "Share enough information to answer questions, but don't give away so much that you push an investor to say no to the deal."

At the pre-term sheet stage, control access carefully. Use unique, revocable links for each VC — not a shared Google Drive folder. Platforms like SendNow create branded deal rooms with per-investor access controls, NDA gating, and document analytics. You see exactly which documents each VC reviewed, for how long, and whether they shared access internally. This gives you real leverage in the follow-up conversation.

What financial documents do founders need for Series A?

VCs evaluate three things in your financials: does the business work today, will it work at scale, and does management understand the numbers well enough to defend them?

The core financial documents for a Series A data room are:

Historical Financials (3 years or since founding, whichever is shorter)

- Income statement (P&L)

- Balance sheet

- Cash flow statement

- Monthly MRR/ARR breakdown if SaaS

Projections (typically 24-36 months)

- Revenue model with assumptions explicitly stated

- Headcount plan tied to projected growth

- Burn rate and runway calculation

- Path to profitability or next funding milestone

Key Operating Metrics

- Customer acquisition cost (CAC)

- Lifetime value (LTV)

- Churn rate (monthly and annual)

- Net revenue retention (NRR)

- Gross margin by product line

Cap Table

- Full capitalization table showing all share classes, option grants, convertible notes, and SAFEs

- Pro forma cap table showing post-Series A ownership including the new investment and option pool expansion

Underscore VC emphasizes a point that founders frequently miss: "Share the same forecast that you show in board meetings and use to operate your business; don't create a separate one for investors." Investors will probe assumptions. If your investor forecast differs from your operating forecast, the inconsistency becomes a trust problem.

A common error is sharing an interactive Excel model. Instead, share a PDF or slide deck that summarizes the financial story with the key drivers and assumptions. Let investors ask for the model in a follow-up call where you can provide context.

What legal documents are required for Series A due diligence?

Legal diligence covers four risk areas: corporate formation, IP ownership, contractual obligations, and employment. Investors' lawyers look for anything that could create liability, block the financing, or affect value.

Corporate Formation

- Certificate of Incorporation and all amendments

- Bylaws and all amendments

- Board consent minutes (every major decision since incorporation)

- Foreign state qualifications if operating in multiple states

- Current Certificate of Good Standing from the state of incorporation

Intellectual Property

- IP assignment agreements from all founders and early employees — this is the most common gap in early-stage companies

- Any patents filed or pending, with filing documentation

- List of all trademarks registered or in use

- Licensing agreements (inbound and outbound)

- Open source software usage and compliance records

Contracts and Obligations

- All customer contracts above $25,000, especially those with MFN clauses, exclusivity provisions, or anti-assignment language

- Vendor and supplier agreements

- Office lease and any real property agreements

- Debt instruments and lines of credit

- Any change-of-control or co-sale provisions in existing investor agreements

Employee and Equity Documents

- Offer letters with equity terms for all key employees

- Confidentiality and IP assignment agreements (every employee, every contractor)

- Equity plan documents: stock option plan, option grant agreements, exercise notices

- Any pending equity grants that have been promised but not yet documented

Pitching Angels' investor data room guide notes a pattern attorneys watch for: "Most deal delays we see come from unsigned IP assignment agreements, not from financial complexity. A founder who wrote the codebase and never signed an assignment to the company creates a real problem."

YC's checklist also contains a specific warning about pending equity grants: finalize all promised grants before you start raising. A term sheet creates a material event that may invalidate your current 409A valuation, forcing new hires and early employees to receive options at a higher strike price.

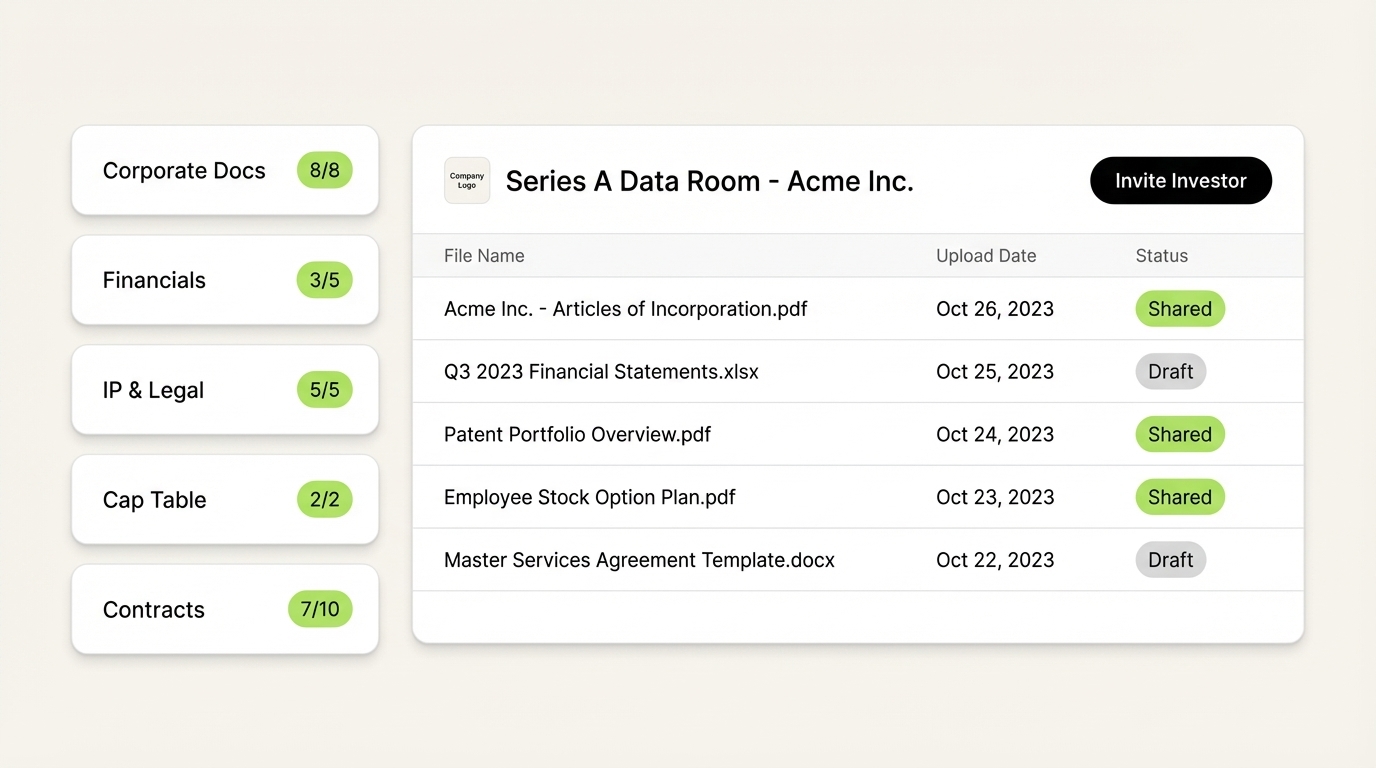

How do you organize a due diligence data room?

Organization is a signal. Investors and their lawyers form impressions from how your data room is structured before they read a single document.

Underscore VC's guide quotes a partner directly: "I assume you run your company like you run your deal room. Are you clear and professional, or careless and sloppy?"

A well-organized Series A data room uses this folder structure:

Keep Reading

- The complete due diligence checklist for seed and Series A startups raising a funding round. Know exactly what documents investors request, how to build your data room, and how to close faster.

- M&A Due Diligence Checklist: The Full 2026 Guide

- Virtual Data Room for Startups: What You Actually Need

- How to Know If an Investor Opened Your Pitch Deck